The State Of Indie Beauty 2022

About a year later, Moss was generating as much as $60,000 in monthly sales. It entered a handful of small clean beauty retailers and e-tailers such as Integrity Botanicals, Aurora Beauty, The Green Jungle Beauty Shop and Seed to Serum, which shuttered in 2017, but customers mostly shopped for Moss on its website, where they connected to Brozek, and she could realize better returns. In 2018, she introduced a lower-priced line called Ambar.

“It really felt so effortless. I’m making this cool stuff, and everyone is like, ‘Great, let me have it.’ It was the easiest thing in the world. I don’t even know if I had any expectations for it or that it would even become what would solely sustain me. It was really for my own skin that I was doing it,” says Brozek. “I really think it’s not normal for it to happen as effortlessly as it did.”

Whether the conditions at the outset of Moss were normal or not, they’re certainly not the same seven years later. Running an indie beauty business in 2022 is rarely effortless. Instagram has increasingly become a pay-to-play environment. Apple’s iOS 14 update slashed the efficiency of social media advertising. Supply chain disruptions and soaring costs have eaten into margins. Omnichannel distribution requiring brands to support an array of channels has become the preferred distribution model. The indie beauty segment has been flooded with both passion-driven brands like Moss and opportunistic brands driven by profits over passion.

Amid personal and professional shifts, Brozek, who had two children after Moss launched, has decided to close Moss on June 8 and move to astrological coaching full-time at her newer ventures Stellar Parenting and Surf + Stars Social Club. Asked about her decision, she says, “I think about what would have happened with Moss if I hadn’t been parenting so intensively at the same time, but Instagram did change a lot, and the market began to saturate pretty quickly. I think it was a combo of all three.”

Moss isn’t alone in closing. In the last several months, Makeup Geek, Steel Birch, Hush + Dotti, Redbudsuds, Woodlot, Sigil, SaltyGirl Beauty, Good Beauté and Evenprime have joined it in closing or announcing they will be closing soon. While it’s tricky to verify if the number of beauty brand closures is swelling, indie beauty entrepreneurs are confronting a remarkably tough landscape—and several have stepped away because they’ve determined their brands can’t succeed in it or they aren’t as enthusiastic about steering them as they once were.

Lauren Leibrandt, leader of the beauty and wellness practice at investment bank Baird, believes it may be the most difficult stretch in recent history to operate a small beauty brand. “You have this conflation of factors on a macroeconomic basis like inflation and supply chain issues that are a real concern for a small beauty brand,” she says. “If you have to pay a lot more or if your product is delayed or you are running into a ton of headwinds on the supply chain side, it can further exacerbate what is happening to your bottom line.”

Small beauty brands are being squeezed as new brands unrelentingly materialize. Some older brands are undoubtedly pushed out by competition. “As many brands that there are closing, there are even more launching, so it’s harder and harder to find a point of difference, especially when you have a limited budget,” says Andrew Glass, founder of skincare brand Non Gender Specific, and co-founder of skincare brand Joos Cosmetics, waxing product brand Wakse and branding agency Pradrem.

Rachel Roberts, founder of beauty brand marketing firm Oyl + Water, predicts closures will climb in the near term as beauty companies struggle to gain footholds. “I feel like sales are slower now than they’ve ever been,” she says. “Even though the recipe for launching brands has stayed the same, and it leads to a successful brand launch, if you are looking at the first six or nine months, the sales have slowed. So, what’s the reason for that?” Responding to her question, Roberts says, “Attention is just diverted among way more brands.”

Brand closures may also climb as a result of a weak appetite for distressed assets bolstered by mounting fears the United States could plunge into a recession. Discussing distressed beauty brands, Ashleigh Barker, head of beauty and director in the consumer group at investment bank Lincoln International, says, “It’s tough to keep up with the current supply chain issues. If they can’t serve stores with inventory, they’ll have stockouts, which means stores are going to replace them. Once you’re out, it’s hard to get back in. At the end of the day, you run out of money and, even if it’s the most beautiful brand, investors want to buy growth. They want upside.”

The sorts of indie brands making inroads in the market today tend to be different than the sorts of indie brands that made inroads a few years back. They’re regularly well-funded brands, frequently associated with celebrities, influencers or entrepreneurs with prominent track records, with the wherewithal to pay the loftier costs of inputs and ads, and provide retailers with confidence they can fuel sales. “I don’t think you can be a scrappy bootstrapped indie brand and expect to make it in the first year anymore,” says Roberts. “I think you have to come to the party knowing you may not make money in year one and that you can survive that.”

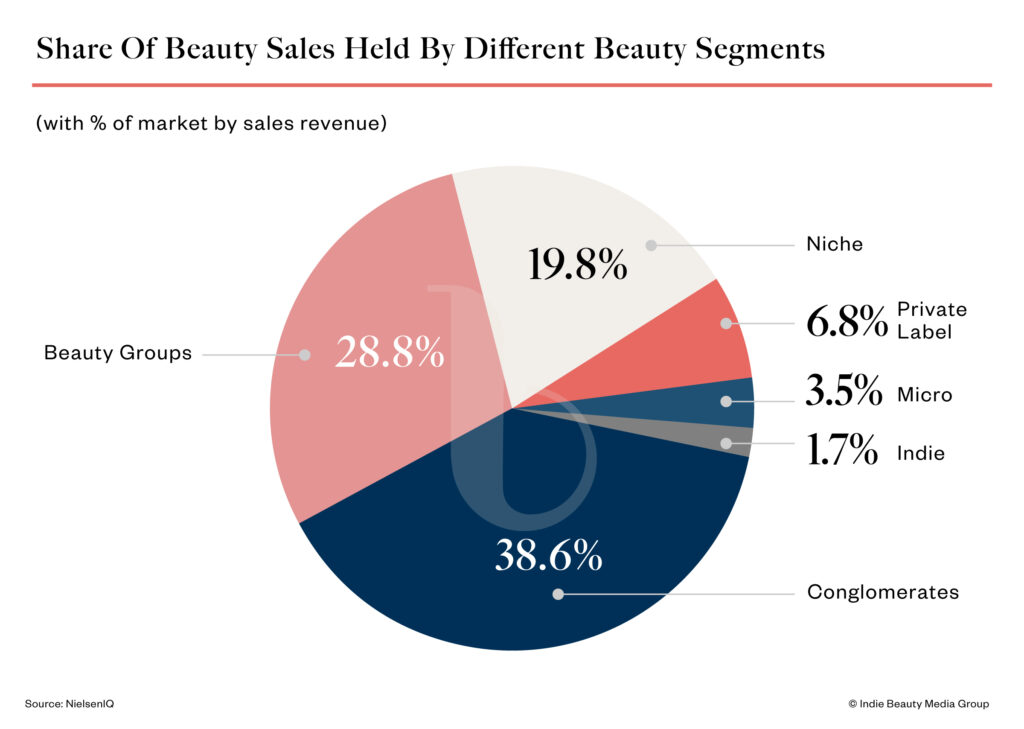

Despite the steep challenges, there remains a case for optimism on the indie beauty front. According to NielsenIQ, consumer demand for indie beauty was strong as the pandemic spread in the U.S. In a report delving into indie beauty from 2020 to 2021, the measurement and analytics company finds it was the only segment to best the market in sales, unit and velocity growth. NielsenIQ defines indie beauty as containing independent, small-scale and fast-growing brands. Examples of indie brands it gives are Pacifica, Pixi, Milani, Aztec Secret and Olive & June. Indie generated 1.7% of beauty sales in 2020 to 2021, but punched above its weight as it accounted for .6% of total brands.

Other segments NielsenIQ tracks are conglomerates (e.g., Neutrogena, Suave and Olay), beauty groups with extensive portfolios that aggressively acquire (e.g., E.l.f., Revlon and L’Oréal), niche brands zeroing in on specific slices of the market (e.g., Banana Boat, Dr. Teal’s and Scunci), private-label brands manufactured by retailers and micro brands under $1 million in revenues (e.g., Clutch Nails, Difeel and Sea & Ski). Across an analysis of 7,000-plus brands, the segments held, respectively, 38.6%, 28.8%, 19.8%, 6.8% and 3.5% shares of beauty sales from 2020 to 2021.

NielsenIQ concludes, “Our data shows that indie and niche brands outperformed during the pandemic and will likely dominate the recovery suggesting conglomerates and beauty groups will continue to lose share.” The rosy outlook for indie beauty aside, indie beauty brand founders generally report the road ahead appears particularly uphill. Below, Beauty Independent takes a deep dive to decipher the market forces hampering their businesses—and identify grounds for hope.

Now scheduled to launch in June, the clean fragrance brand Eauso Vert’s debut has been postponed nearly a year due to unexpected costs and supply chain delays. Its manufacturer pushed up its minimum order quantity from 5,000 to 10,000, and Eauso Vert altered the design of its secondary packaging due to lack of material availability. The brand is still waiting on cork caps from Spain.

“Some manufacturers were uncertain as to whether there would be repeat orders from brands, so they didn’t hold any stock, which led to longer lead times on the materials, so it goes around in this circle of delays,” says co-founder Faye Harris. “You’re kind of at the mercy of your suppliers and what’s available.”

Eauso Vert’s supply chain problems aren’t unique. They’ve ravaged the beauty industry since the start of the pandemic. The war in Ukraine, China’s lockdowns and spiked gas prices have exacerbated the problems. The supply chain snags disproportionately impact indie brands with scant resources.

The prices for plastic-free haircare brand Dip’s paper packaging have jumped 30%. Founder Kate Assaraf has chosen to absorb the increase out of worry her customers might balk at heightened prices. She says, “When the Dollar Store increased its prices, people went crazy.

Robyn Watkins, founder of product development company Holistic Beauty Group, divulges the price of aluminum tubes have increased by 30% as brands opt for plastic alternatives, and MOQs for them have risen from 10,000 to 25,000. She says, “There’s a shortage, and demand is high so manufacturers are telling brands, if you can’t meet this MOQ, then we’re going to give it to somebody who can.”

The companies able to afford elevated costs, not the most cash-strapped indie beauty companies, are amassing safety stock, compounding cash-strapped brand’s troubles accessing supply. “They can actually go to the raw material suppliers and say, ‘Hey, I know that sunflower seed oil is be becoming affected in the supply chain because of the war in Russia, but here’s my forecast for 2022, please make sure that you go out and you get it and you stock it for me—and here’s a check for that,” she says. “There’s no raw material security unless you pay for it, and you plan for it, and you forecast against it right now.”

The smaller brands that can are trying to place larger orders of materials than usual in order to negotiate lower prices, but the strategy comes with risks. Délali Robinson Cosmetics’ manufacturer, which it’s been a client of since 2016, tripled its minimum order quantity this year. Founder Adodo Robinson said, “The struggle became, do I raise my prices and risk losing my base clientele or should I order more inventory?” She decided on the latter. “Now, I’m sitting on all of this inventory, which is taking double the amount of time to move,” she says.

Pursuing a similar course, Assaraf placed a big bulk purchase order for Dip’s merchandise in a bet that inflation will persist and mitigate out-of-stocks in the summer, a peak selling season for the brand. “I’ll be running on fumes for a little while hoping that it’ll pay off later,” she says. Assaraf had to deal with out-of-stocks for two weeks during Earth month, another busy time for Dip, and is aiming not to repeat that experience.

The out-of-stocks are especially detrimental for small brands. Eric Korman, CEO of contract manufacturer The Goodkind Co., says, “Unlike a large brand or conglomerate, where out-of-stock positions could mean missing expectations for a quarter, which is frustrating, but not company ending, for indie beauty brands, a long out-of-stock could mean literally running out of their oxygen, cash.” When indie brands have out-of-stocks, Watkins says, “I can see a retailer being like, ‘Oh, we could have given the slot to a P&G brand, they wouldn’t have let us down.'”

To prepare for supply chain issues, Watkins’s main tip for indie beauty brands is that they hire forecasters to help them plan about 18 months ahead. “Even if it’s a freelance finance person, get someone to look at your business to help you understand what the big bets are and plan against that,” she says. “It does come down to having resources, but it also comes down to planning.” For brands that have funding, she recommends them pouring it into their supply chain. Watkins says, “Put resources behind that versus just focusing on marketing and social media.”

Melody Bockelman, founder of beauty brand development consultancy Private Label Insider, advises brands to have backup manufacturers that they can resort to if there’s shutdowns or exorbitant delays. “You don’t want just one supplier, you need at least three,” she says. “And you may say to yourself, I’m private labeling, but find a formula that is similar enough that, in a pinch, you can roll it out temporarily.”

More manufacturers and suppliers are relocating from Asia to North America. Glass counsels brands to streamline their supply chains and keep their vendors local. “Instead of having a formula made in Italy because it sounds bougie, have it made in the U.S.,” he says. At Non Gender Specific, he adds, “I work with three vendors from formulation to packaging, and I did that because it’s much easier to do and build relationships with those companies.”

In the Great Recession, Bockelman says brands that supersized their products made a mistake. The ones that did the opposite stuck around. She says, “They understood what is actually selling, and they got lean and cut everything,” she says. Brands that released trial sizes and tools to enhance value and increase order rates stuck around as well.

Bockelman anticipates the supply chain crunch will contribute to a “shaking out” of the beauty industry. “Founders are going to have to decide how much they really want to be in it and whether it’s a hobby or a business,” she says. “When we’re talking about supply chain, what makes you stay ahead of it is having that capital to buy it.”

The direct-to-consumer wave was a boon to indie beauty brands. At its nascent stage, it allowed them to establish an identity, attract sales without retail middlemen and obtain customer insight at relatively low cost. These days, indie beauty brands face tens of thousands of dollars a month in pay-per-click (PPC) advertising and social media marketing charges as the returns from Facebook, Instagram and Google ads diminish in the wake of the iOS 14 update. The expensive digital dynamics have pushed brands to retail—and retailers have played ball in a desire for newness to attract young shoppers.

“A big shift that has become apparent in the indie beauty scene is the fact that major retail has decided to step out of its traditional hands-off role to now becoming an active participant in guiding and nurturing independent brands,” says Mia Bell, founder of consultancy Inspired Beauty Wholesale. “From providing small business grants to bringing visionary founders into specialized brand accelerators, retailers are investing their resources into championing indie beauty.” Retailers as divergent as Sally Beauty, Credo and Bluemercury have championed indie beauty, but the indie beauty segment is missing covetable retailers like Barneys New York and Colette that were havens for chic upstarts.

While there’s absolutely room for indie beauty brands at retail, cash-strapped brands have to contend not only with legacy brands, but with new brands either from large corporations or backed by substantial investment that they may not have had to contend with in the past. For instance, Unilever has been spun out Ferver, a fermented skincare brand sold at Target, from its incubator The Uncovery, and Procter & Gamble created gen Z haircare brand Nou for Walmart.

The latest entrants into Ulta Beauty’s Sparked program for up-and-coming brands are buzzy VC-backed brands Hally and Vacation, Tresluce Beauty, a brand from singer Becky G and Ipsy’s incubator Madeby Collective, and Sk*p, an eco-friendly skincare and haircare brand by Mark Veeder, co-founder of Farmacy. The Outset, the clean skin brand linked to actress Scarlett Johansson, freshly rolled out across Sephora’s doors in the U.S.

“What retail sourcing ultimately comes down to is this, ‘Which brand has the specific product that can fill that specific gap in our assortment?’ Should it happen to be a VC-backed brand that can fill that void, then that’s where their choice will fall,” says Bell. “Bootstrapped brands can and have been able to succeed in major retail environments. If they simply have an understanding of what would be required of them in such environments and be prepared to execute on those requirements, then they too can thrive.”

Once bootstrapped brands score major retail partnerships, they may not be prepared for the costs and commitments they stipulate. Retail brokers can charge up to $15,000 a month to get brand’s foot in the door, and retail expansion can cost hundreds of thousands of dollars in sales and marketing support, depending on the retailer and number of doors. Brands often have to seek outside funding to make large retailers doable.

“Indie brands are holding on as long as they can before they have to ask for money. They don’t want to give their brand up to anyone,” says Paula Floyd, founder of beauty sales and education firm HeadKount. “But the truth is 40% of brands—indie or not—get exited in retailers. Eighty percent of that 40% is because they didn’t support retail.”

She continues, “The indie brands that are winning at retail are the ones focusing on the doors where they’re succeeding and then growing from there. There’s a 3-6-9 month mark that’s really important for a brand at the beginning of its retail life cycle. You start small and, at three months, you’ve hit a certain target in a small group of stores. Then, you broaden and take everything you learned from the first benchmark and open in say 20 more doors. By six months, you’ve hit another target. By nine months, another and so on. It’s a much better strategy than opening in 600 Ulta doors all at once and trying to support all of them. You’re throwing your money away, in my opinion.”

Indie brands looking to grow their digital presence are leaning on expanding e-tailers for distribution. Strategic growth firm KSJ Collective spotlights e-tailers Thirteen Lune, NakedPoppy, Safe & Chic and Integrity Botanicals as supporters of indie beauty. Unafraid to invest in emerging brands, these platforms can kick off a brand partnership with healthy opening orders and reorder monthly.

The metaverse is a virtual ecosystem that indie beauty brands should consider, according to Taylor Barry, co-founder of beauty brand consultancy Beauty Breakthrough. Large beauty brands like MAC, Clinique, Charlotte Tilbury, and Tatcha have begun to experiment with virtual pop-ups and storefronts to stoke customer engagement and awareness. “We’re speaking with one of our brands now about how they can be an early adapter to this new concept,” says Barry. “There’s this move to what is being called ambient retail now, which is a state of retail being everywhere, woven into social and entertainment experiences. It’s going to become a whole new way to play in beauty.”

Less virtual, Glass highlights hospitality and travel retail as distribution and marketing avenues for indie beauty brands that haven’t been fully exploited. Travel retail is responsible for around 20% of Non Gender Specific’s sales. The brand exhibits at the trade show TFWA World Exhibition & Conference to get in front of travel retail companies and uses the agency Harper Dennis Hobbs to assist it with participating in airplane shopping. Glass says, “In travel retail, they do want established brands with a sales history, but, if you have some good retailers and press under your belt, you have a good chance.”

Social media has upended the beauty industry, making the enterprise of indie beauty more capital-intensive than ever. When Tara Foley opened Follain in Boston in 2013, she discovered brands on Etsy and at local boutiques. She spotted Herbivore on Etsy and Ilia at a clothing store. Now, buyers are scrolling social media to hunt for brands.

“Brands are built for social media,” says Foley. “They’re not built the way they were—product first, ingredients first, distribution first. To build something for social first, it requires a lot more resources. There are a lot of lookalikes for what’s on the inside of the bottle because people are most focused on the follower count.”

Although indie beauty brands are being catapulted by TikTok fame, Ransley Carpio, co-founder of incubator Patina and head of venture investments at Fortress Brand, views beauty products going viral on TikTok and the stickiness of the gen Z customer with skepticism. “I’d be a little bit worried as a brand because the rise would be so insane that I wonder how fast the fall is,” he says. “How much meaningful sustainable revenue is gen Z creating for these brands?” Already, indie beauty brands have “very low” customer loyalty and “very high” shopper churn compared to larger mature brands, according to NielsenIQ.

Clean beauty, initially regarded as dangerous territory for legacy brands, handed indie beauty brands an open category to flourish in. Contemporary consumers are keenly interested in clean beauty. Per a Piper Sandler survey of gen Z consumers, 60% of females read beauty product ingredients, 88% would pay more for “clean” and 58% would pay more for “science-backed” products. However, the clean beauty category has become inundated. Almost all brands arriving on the market are positioned as clean, and indie brands can’t tout their clean formulas as a distinguishing characteristic.

Last year, market research firm The NPD Group found clinical skincare brands contributed the highest revenue leaps in prestige skincare. Indie beauty brands can definitely be in the clinical skincare field, but it’s commonly pricier than clean skincare. Ultimately, Foley thinks consumers want brands to be both clean and clinical, a combination dubbed “cleanical.”

“They’re asking us for ingredients and packaging that are better for people and the planet, that has to be there, but then it also has to have extremely high performance, proof of performance, clinical trials and side by sides with other products,” she says. “They’re like, ‘Show us the proof.’” She elaborates, “The next generation is highly aware of who they are in terms of their skin type and concerns, which I think is unique compared to millennials…They live in this world of algorithms, and they’ve come to expect a personalized approach for what they need. From there, they want brands to offer the highest standard possible. That forces brands to move at a rate that I think the industry is right now really uncomfortable moving at, but is trying.”

The indie beauty shakeout occurring may be at least in part due to a transition away from skincare. Indie beauty brands proliferated in the skincare category, although, overall, NielsenIQ’s data underscores they’re under-penetrated in skincare relative to their larger rivals. With skincare growth softening, brands in the category are suffering. Still, there’s potential for indie beauty brand explosions in other categories. NielsenIQ observes indie beauty brands are under-penetrated in hand and body lotion, and haircare, a category that’s in a high-growth cycle and has yielded transactions of late.

Barker singles out brands with functional benefits as poised for growth. She says, “Functional beauty, i.e., having a purpose or benefit beyond what the product appears to do on the surface which could be tied to hormonal balances, mental wellbeing, etc., these categories are ripe for innovation and new consumable formats that consumers actually want to see.”

Carpio is bullish on the once-sleepy over-the-counter (OTC) category. Indie beauty brands are waking it up with modern offerings. Previously, Carpio says, “If you had something that you needed to fix, you probably went to get a prescription filled by some professional. It came in this really sterile packaging, and you were probably hiding it. Now, these products are coming out and creating messaging, values, packaging and really empowering the folks that have these issues.”

With gen Z and millennial consumers mainstreaming cosmetics procedures, Roberts is watching brands spiff up pre- and post-treatment products. Carpio, Roberts and Barker suggest brands can hop into categories that are being destigmatized. Women’s wellness sectors fall into this arena as does psilocybin or compounds from hallucinogenic plants. Referring to psilocybin, Roberts says, “I will be interested to see how that makes its way to beauty and wellness. We are seeing beauty and wellness continuing to blur together, even skincare brands are having conversations that’s not really about what you put on your skin, but how you live, eat and feel.”

Barker, Leibrandt and Roberts emphasize ESG-oriented (environmental, social and governance) indie beauty brands may be able to deliver on commitments their corporate counterparts can’t deliver on. “Sustainability, environmental mindfulness as well as gender and race inclusivity are all attributes that are no longer nice-to-haves, but must-haves in the eyes of consumers,” says Barker. “Emerging indie brands have been able to authentically convey these values from the start and will be well-positioned to take share from incumbents who are adapting to, but not leading with, these values.”

There’s probably no returning to the “magical” indie beauty period in the 2010s. What Foley is wistful for is passionate indie beauty entrepreneurs like April Gargiulo of Vintner’s Daughter. In their stead, celebrities and influencers with massive audiences, but typically limited product knowledge, have been the voices and faces of beauty brands.

Foley knows the fascination with celebrities and influencers in beauty may not subside, but wants founders to get their flowers, too. “I hope to see a movement where consumers want to go back to learning more about the people behind the brands. These are some of the most innovative leaders in the space and they definitely deserve a lot of credit,” she says.

As unlikely as it may seem with her skincare brand coming to an end, Brozek isn’t despondent about the state of indie beauty. In fact, she argues beauty entrepreneurs can overcome the current challenges.

“It still feels like having an authentic energy and that belief in your brand is really important. It doesn’t really matter what the landscape looks like, I think that can take you a long way,” she says. “It’s a more crowded space. Advertising and getting the word out is more expensive, but, even still, humans are creative and resilient, and I think, if someone is really scrappy, they can be creative in different ways to build their brand and get the word out.”

The players

5 mentionedTatcha

Neutrogena

Clinique

Harry's

Vacation