The Wellness Multiplier: GLP-1s, Aesthetic Procedures And Health Prioritization Accelerate Sales

“There’s an opportunity for premiumization,” says Anna Mayo, VP of the beauty vertical at consumer intelligence firm Nielsen IQ. “People are willing to pay more for products that are better quality and that are offering them more benefits.”

During a webinar hosted by entrepreneurial network Naturally New York last month, Mayo shared recent NIQ research highlighting the explosive growth of wellness-driven beauty categories, the expanding impact of GLP-1 drug use across beauty and wellness, and the brands and channels gaining ground in the wellness-first ecosystem. Below, we break down actionable takeaways.

The Wellness Sales Rush

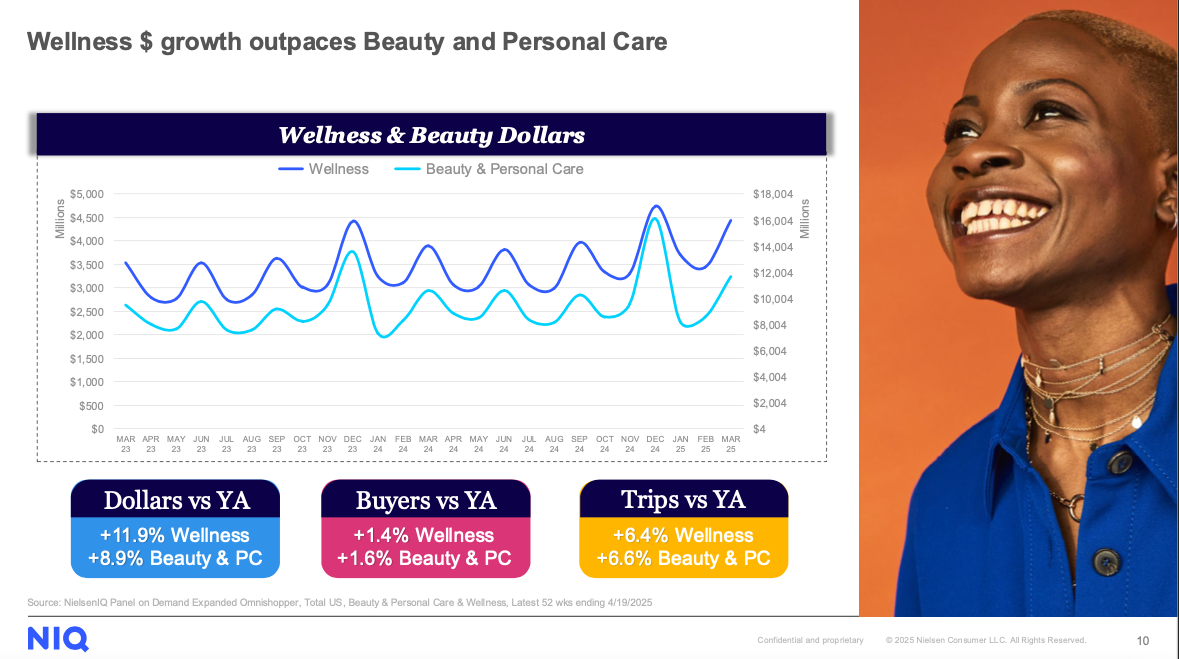

Over the past two years, the growth of wellness has outpaced beauty and personal care, the former rising just under 12% and the latter just under 9%. But, in 2025, it’s hard to fully disentangle beauty from wellness, and it’s becoming clear that the hybrid category is greater than the sum of its parts. NIQ found that, while the total beauty and personal care market is around $120 billion, adding in beauty-adjacent wellness categories bumps the market up to $160 billion, a 36% increase.

The bulk of wellness’s growth is driven by supplements, but there’s also strong sales potential in oral hygiene, home fragrance, period care and sexual wellness. Mayo says, “These are categories that we think have a natural affinity with existing beauty and personal care brands and retailers for expansionary opportunities.”

There’s a striking dynamic emerging between online and in-store beauty and wellness shopping. Currently, about 46% of beauty and personal care sales are happening online, but that share is climbing. Online sales growth is about 20%, and in-store growth is only 1.2%. The online share of both wellness and beauty sales are hovering around 50%. Sexual wellness and supplements are reaching 60% in terms of online as a share of total sales. In contrast, in-store sales still occupy the commanding share of fragrance, oral care and period care.

Mayo says, “A lot of people want to understand the scent and be actually able to smell it before they purchase it, as well as oral hygiene and femcare, which are those ‘needed now’ categories that remain majority in-store.”

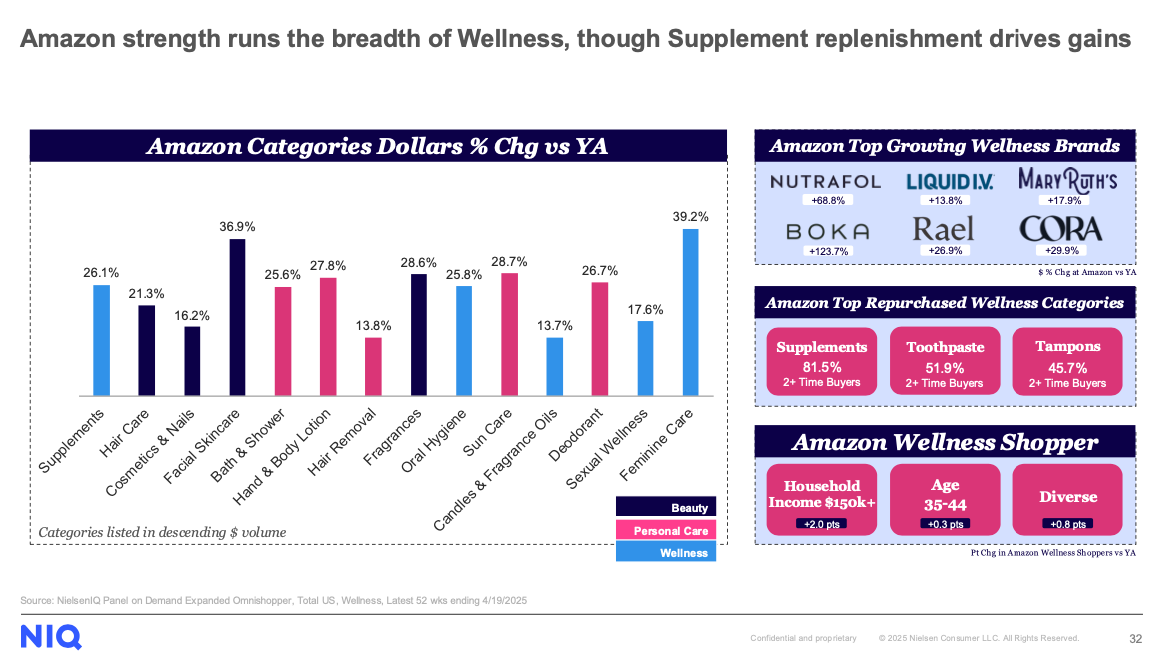

The interplay of—and differences between—in-store and online commerce is paramount. Amazon dominates online sales and has been registering double-digit gains across beauty, wellness and personal care. Facial skincare and femcare are the two fastest-growing categories, but supplements are growing fast, too, at about 26%. Leading brands include Nutrafol, Liquid IV, MaryRuth Organics, Rael and Cora. Still, NSQ data shows drugstore chains like Walgreens and CVS hold the strongest association with wellness for consumers, followed by Target, Amazon and Walmart.

For brands, Mayo instructs, “Thinking digitally first has become critical, understanding how people shop the digital shelf versus the physical shelf and how to adapt brand strategies for that.”

In the physical retail realm, Mayo spotlights Ulta Beauty’s efforts at repositioning what it stands for as not just a beauty merchant, but as a wellness destination as working to widen its opportunities for sales. “They’ve actually taken out shelf space from their traditional beauty products to make room for wellness,” she says. “We’re seeing body care, deodorant, sun care and supplements perform really well in Ulta.”

The Transformative Effects of GLP-1s on Beauty and Wellness

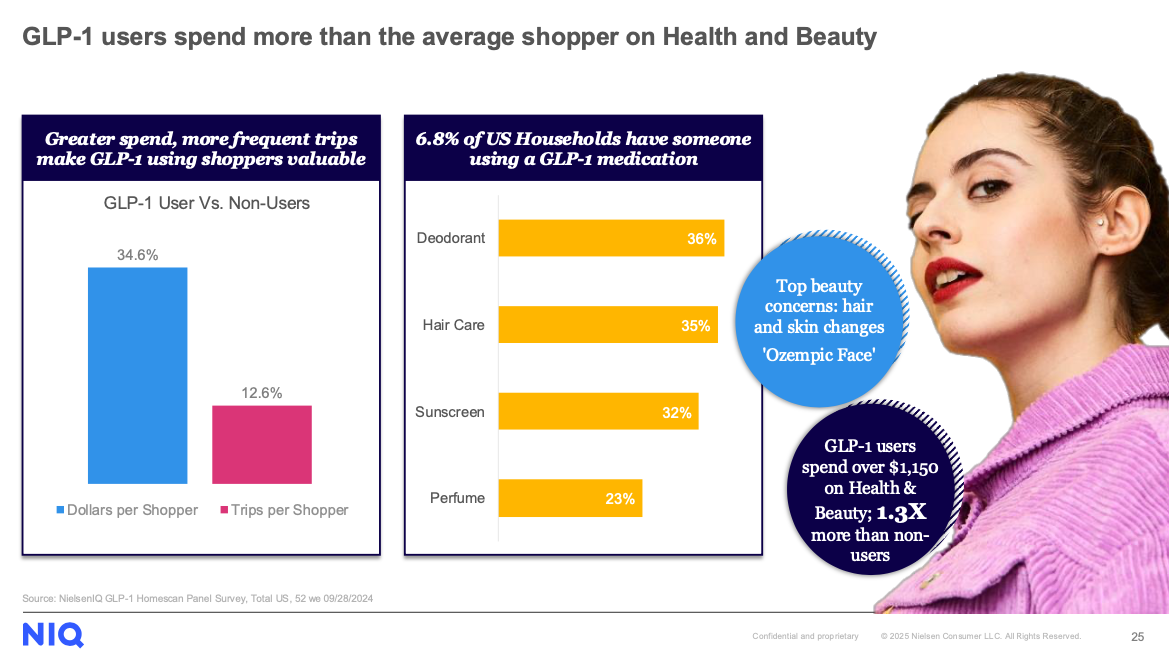

Health policy research organization KFF estimates 12% of Americans have used GLP-1s, and NIQ estimates 7% of households in the United States currently contain someone using a GLP-1 medication. With the drugs’ rapid proliferation, consumers are putting weight loss, nutrition and exercise goals at the top of their wellness priority lists.

According to NIQ, more than half of North Americans say that maintaining a healthy body weight and improving heart health are more important today than five years ago, and 32% would consider using a weight loss drug if recommended by a healthcare professional. Fifty-five percent say healthy nutrition is more important to them now than five years ago, 22% hold a very negative view of ultra-processed foods and 56% plan to increase their amount of physical exercise in the coming year.

GLP-1 users tend to be heavy health and beauty buyers. NIQ found that they spend about 30% more than non-GLP-1 users on health and beauty. Catering to their demand, the amount of products across all consumer goods categories marketing toward GLP-1 users is set to balloon.

“Rapid weight loss can cause changes to the hair, to the skin, and we find people really looking for solutions to help them solve these issues,” says Mayo. “If you go in the frozen food aisle, you’d probably be amazed how many products are calling out on the front of the box GLP-1 support or protein for GLP-1s. Lots of supplements are being released specifically to help boost [a person’s] GLP-1 without a shot.”

Medical aesthetics is experiencing an influx of GLP-1 users. About 63% of GLP-1 patients receive medical aesthetic treatments to address sagging skin from dramatic weight loss and thinning hair.

“They’re taking new trips to see a professional for this,” says Mayo. “This is important because, when we see people take a trip to a medical provider for aesthetic treatments, it does impact their at-home routine. We see a portion of them who actually cut back on their products, switch to less expensive products so that they can make room in their budget to afford the professional treatments.”

GLP-1 users exhibit a significant rise in spending in the first nine months after starting the medication, but those spending levels even out after a year of use. Mayo says, “It is important to capture these people right away, get in as part of their routine because you don’t have the biggest timeframe in order to influence their behavior.”

The players

5 mentionedBetter Being

Under Your Skin

AS Beauty

Nutrafol

Ultra