Can Masstige Beauty Keep Its Mojo?

In recent months and years, though, the mid-tier segment has burst into the spotlight. Across prestige, masstige and mass beauty, Circana estimates masstige posted the largest dollar jumps in beauty for 2023 and 2024 so far. It commands only 10% share of beauty sales in the United States, but brands in it such as Naturium, which was acquired by E.l.f. Beauty for $355 billion last year, Good Molecules, The Inkey List, Bubble, Odele and Byoma, which is up for sale, according to the publication Axios, have experienced outsized success.

They’re being snapped up by increasingly savvy consumers who understand that “quality and affordability can be synonymous,” says Linda Wang, founder and CEO of Karuna and Avatara, a masstige skincare brand carried by Target. “With all the advances in cosmetic formulations and a less wasteful approach to packaging, effective skincare doesn’t have to and shouldn’t break the bank.”

Whether masstige’s success will endure is an open question, with those contending it will citing the social media push for products that punch above their price, consumer frugality, formidable brands and the impact of younger consumers without the discretionary income of their parents and grandparents, and those contending it won’t underscoring that an onslaught of players are jockeying to triumph in a masstige arena that remains miniscule and squeezed consumers will descend the price ladder in mass.

Wang is on the side of masstige’s momentum sustaining. “It’s not going anywhere anytime soon and for good reason,” she says. “There are so many great developments in the industry—I see new ones every day—that lend themselves to helping brands create really unique, benefit-driven products that don’t need to come with a hefty price tag.”

Marc Elrick, CEO and founder of Byoma, concurs, reasoning that brands like Byoma have blunted the impetus to spend lavishly on skincare. “Today’s consumer no longer believes price has a direct correlation to efficacy. With the rise of TikTok ‘dupe’ culture, consumers, especially gen Z, are more aware and focused on value…Prestige consumers will trade down while mass consumers will trade up when efficiency and results are delivered without the premium price tag,” he says, predicting, “Masstige will continue to grow as consumers shop both high and low based on product need.”

The term “masstige,” a portmanteau of prestige and mass, conjures up beauty products emulating the ingredients, brand copy and design of their premium counterparts, but not their premium prices. Epitomizing beauty’s blurring retail channels and shopping patterns, masstige brands straddle prestige and mass distribution, segments it’s been outpacing.

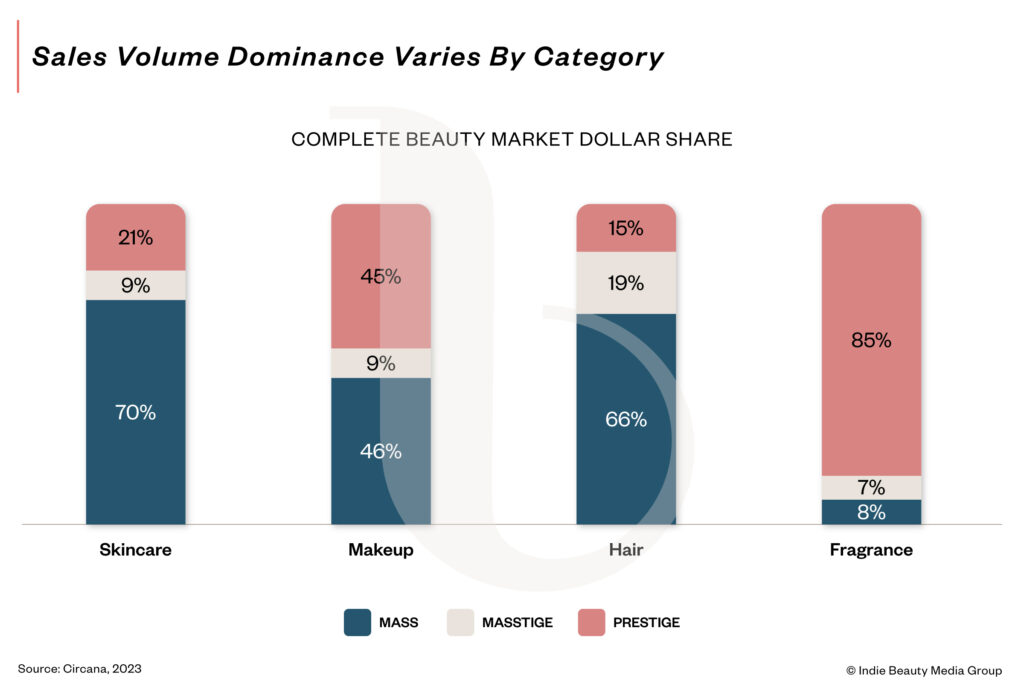

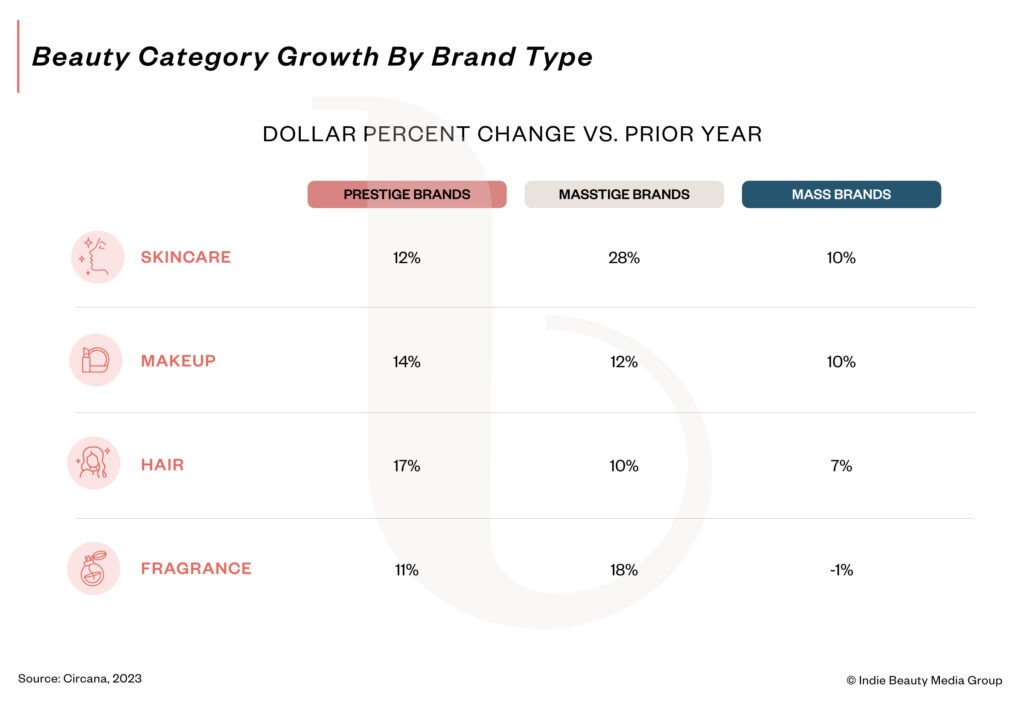

In the first quarter of 2024, masstige sales were up 16%, bettering prestige at a 15% pop and mass with a 3% bump, per Circana. Masstige sales escalated16% in 2023 over the year before. Prestige escalated 12% and mass leapt 9%. At 28% growth last year compared to the prior year, masstige skincare, representing a 9% share of skincare sales, is the subcategory that’s risen the fastest.

“Skincare brands have been able to bring the same exact high-performance active ingredients found in prestige such as hyaluronic acid and retinol, but at a much lower cost,” explains Scott Kestenbaum, chief growth officer for beauty brand incubator Maesa. “They are also often providing robust dermatological endorsements and science-backed clinical testing to substantiate the formula efficacy.”

Rachel Martin, founder and CEO of consumer research firm RemCal Insights, reasons, “As a consequence of the pandemic, consumers became more thoughtful about the products they use. They are no longer willing to pay for marketing [and] nice packaging, and they want to look deeper into the quality of production and ingredients that go into the making of the products. That’s why it’s no longer enough for brands to just have a premium price point to be perceived as effective.”

Hair is the largest masstige subcategory, with a 19% of haircare sales last year. It’s characterized by brands that tout salon quality in mass-market distribution. Masstige haircare sales surged 10%, mass haircare sales were up 7%, and prestige haircare sales rose 7% last year.

Fragrance is the smallest masstige category, with a 7% share of 2023 fragrance sales. Masstige fragrance has been on an upward trajectory as well, with sales advancing 18% versus a 11% jump for prestige fragrance and a 1% decline for mass fragrance last year. Masstige skincare represents 9% of skincare sales, and masstige color cosmetics similarly represents 9% of color cosmetics sales.

Retailers attribute masstige fragrance’s climb to the popularity of dupes and light sprays. Nest’s masstige-priced body mists at $39, along with scent upstarts like Sephora-sold DedCool and Target’s Fine’ry from Maesa are propelling masstige fragrance.

The term “masstige” emerged in the 1990s, but gained recognition in 2003 with Michael Silverstein and Neil Fiske’s publication of “Luxury for the Masses” in the Harvard Business Review. It quickly became a staple in the beauty industry lexicon, embraced by brands like NYX, Pixi and Soap & Glory to articulate their positioning between mass and luxury.

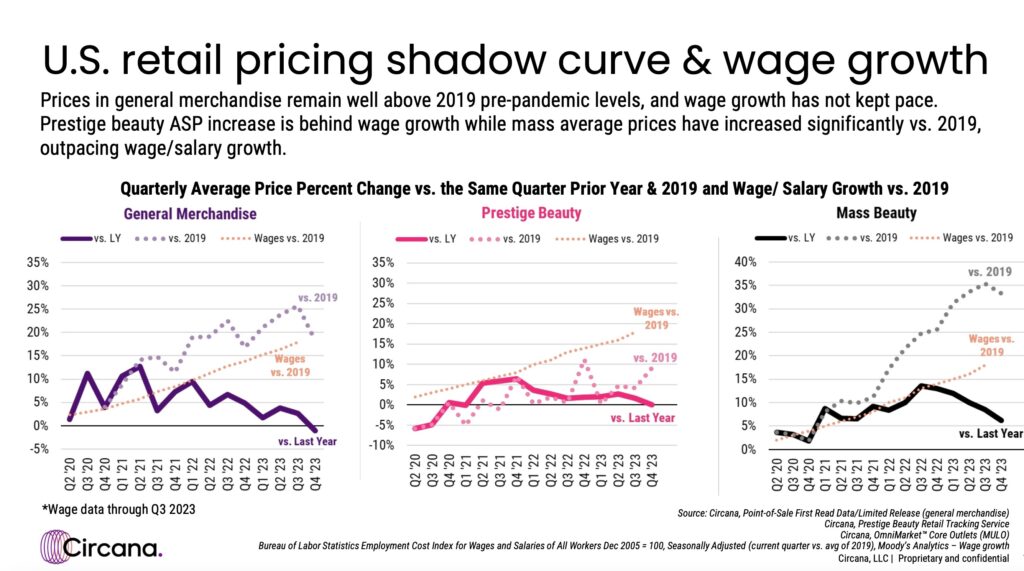

The term has become fuzzier, but generally the beauty industry pegs masstige prices at $15 to $25 for skincare, $10 to $20 for haircare and $10 to $20 for makeup. In the beauty industry widely, Circana has been tracking a significant rise in the average price of mass-market beauty products since 2019. It’s accelerated faster than wages due to inflation and the traction of products with higher prices in mass distribution. In mass, Olay Super Serum is priced from almost $30 to $35. The Ordinary’s steepest product in prestige distribution at Sephora is the largest bottle of its Multi-Peptide + HA Serum at $33.80.

For many in the beauty industry, masstige is more a vibe than a delineated beauty sector, and there are products that tend to be considered masstige despite not squarely situating themselves at the midpoint of mass and prestige. In addition to Byoma, Naturium, Odele, Good Molecules and The Inkey List, brands defined by industry insiders as masstige include The Ordinary, La Roche-Posay, Redken, Bubble, Native, Lume, Kristin Ess, Boots and Glossier.

Celebrity beauty brands, excluding high-end examples like Skkn by Kim, are usually viewed as masstige along with private-label brands. On vibes, some in the beauty industry place brands doing dupes in the masstige lane because they have a higher end valence. Even E.l.f. Beauty, priced in the mass-market range, is judged to be masstige by a few.

“E.l.f. is sold in mass channels, but its narrative is increasingly sophisticated and strategic. Their recent acquisition of Naturium illustrates this evolution,” says Tina Bou-Saba, an early-stage beauty and wellness brand investor. That narrative has been beneficial to E.l.f. expanding its footprint in masstige skincare, where products average around $18, but are creeping up to the $20 mark and above in mass-market chains.

“No consumer calls your product masstige,” says Jeremy Lowenstein, CMO of Milani, a makeup brand known for its affordable luxury positioning. “Consumers are cross-purchasing.”

As consumers cross-purchase, brands are crossing beauty segments. Prestige beauty brands are getting in on the masstige game by releasing masstige-priced options or changing their positioning to fuel volume and experimentation. Fragrance brand Ascention Beauty has introduced an Astral Elixir Collection of perfume wands priced at $38, contrasting with its pricier $118 perfumes featuring crystals. The wands are designed for travel and to serve as an entry-level product for the brand.

Dermasuri recast its exfoliating mitts after detecting interest in masstige pricing. The pivot to masstige, which happened without a price shift, netted it Target distribution. On its website, Dermasuri’s Deep Exfoliating Glove Body Scrub is $14.99, Deep Exfoliating Face Scrub is $11.99 and Deep Exfoloating Back Scrub is $18.79.

“A thorough examination of the skincare prestige market revealed a landscape where remaining retailers faced challenges such as rumored closures of department stores, financial instability, and imposing high barriers for emerging brands to access their platforms,” says founder Melody Akhavan, adding, “For new beauty brands, the masstige market offers a fertile landscape rich with opportunities.”

Tara Bogna, founder of Lash Spell, maintains the masstige segment has multiple advantages for her lash product brand. “It allows us to cater to a broad demographic, reaching customers who seek high-end quality at a reasonable price,” she says. “This inclusivity fosters brand loyalty and broadens our customer base.”

Vera Oh, co-founder of Voesh New York, says masstige was the best route when she expanded her skincare brand from professional to retail distribution. Voesh New York’s Solemate Heel Repair Balm is $14, Collagen Gloves with Argan Oil Trio is $18, Collagen Socks with Argan Oil Trio is $18, Pedi Moments Lavender Relief is $7, Vitamin C Shower Filter is $29 and Crystal Clear Head-To-Toe Cleansing Soap is $14.

By embracing a masstige identity, Oh says the brand “ensured that our high-quality products remained affordable without sacrificing the values that define us. Through this approach, we should be able to balance between accessibility and excellence, allowing more people to experience our brand.”

In beauty industry circles, a frequently mentioned masstige brand is Bubble, but founder and CEO Shai Eisenman asserts the lines dividing mass, masstige and class aren’t relevant in the contemporary beauty business. “The consumer doesn’t look at it that way,” she says. “It isn’t about mass or prestige, it is where the consumer wants to find us.”

Eisenman highlights that Bubble is growing rapidly. Its sales skyrocketed 300% last year from the year before. Industry sources told media outlet Women’s Wear Daily last year that the brand was projected to hit $85 million in 2023 sales. It has 30% awareness in the United States. Bubble products are available in over 12,000 stores, including at Ulta, Amazon, CVS and Walmart.

On Amazon, masstige is a major force, according to Vanessa Kuykendall, chief engagement officer at Amazon agency Market Defense. “Amazon is the ideal destination for masstige beauty shoppers,” she says. “With over 100,000 beauty brands represented on Amazon, there is no bigger virtual beauty store on the internet than Amazon.”

Market Defense approximates that new beauty products entering Amazon are evenly split between mass/masstige and prestige beauty. Zeroing in on beauty and personal care products launched on the e-tailer in the second quarter this year, of the top selling thousand Amazon Standard Identification Numbers (ASINs), 30% are priced from $15 to $30, 25% are under $15 and 45% are over $30.

Amazon fees present a particular challenge to cheaper products. The e-commerce giant imposes a 15% commission on beauty products priced over $10 and an 8% commission on those under $10. Masstige beauty items incur similar shipping costs through Amazon’s Fulfillment by Amazon (FBA) network. Throw in advertising expenses, and masstige beauty products can face total fees upwards of 40% of their prices, whereas fees for higher priced items typically hover at around 26% to 30%.

The appeal of masstige beauty has drawn new entrants, but there’s a debate in the beauty industry as to whether that’s caused the sector to become too crowded. Larissa Jensen, SVP and global beauty industry advisor at Circana, says masstige beauty is “crowded, but not saturated.”

Margarita Arriagada, former chief merchant of Sephora and founder of luxury makeup brand Valdé, posits that masstige beauty is saturated. “The industry always chases the shiny new objects as opposed to leading and guiding,” she says. “It will work until the pendulum swings the other way.”

At least one industry expert, who asked not to be named, predicted a pendulum swing is imminent. “Retailers are prioritizing profit. We are seeing newness slow in big chains,” he says. “Walmart brought in 90 new brands. Now, most of those brands are out, many even out of business. You need to be able to scale to grow with big retailers.”

Target, too, has winnowed down the number of new beauty brands filtering onto its shelves and dot-comm platform. As nascent beauty brands are being slashed, a handful of masstige beauty superstars are scaling. The source says Lume, for example, is killing it. News agency Reuters reported in March that its parent company Harry’s is nearing $1 billion in sales and is profitable. The source also singled out Byoma, Hero Cosmetics, Olive & June, Amika and Dwayne “The Rock” Johnson’s Papatui as masstige winners.

If the economy stumbles, masstige beauty detractors fear the middle will be under strain. Already, consumers are flocking to dupes and other low-priced products they deem to be delivering effectively equal to premium products, Christine Conway, VP at Cult Capital, an investment firm backing prestige beauty brands Lawless, Act + Acre and Subtl, says, “What’s getting cannibalized is masstige, not prestige. Those middle-priced brands that aren’t offering something that’s innovative, but from a lab and easily replicated, those are the brands that are really suffering.”

In contrast, Raina Vaughan, team leader at sales management firm Team Direct and a former Walmart merchant, argues that consumer caution and any future economic slippage could further benefit masstige beauty. “I believe, given the current inflationary environment, consumers will begin channel shifting from prestige back to mass,” she says. “We are already seeing this at retailers like Walmart. These consumers will continue to seek value and often want what masstige brands offer, better value across efficacy and price.”

Cristina Nuñez, co-founder and managing partner at True Beauty Ventures, an early-stage beauty and wellness venture capital firm, suggests prestige beauty is feeling the effects of masstige beauty leveling up. She says, “It puts more pressure on prestige brands to win over consumers with not only top-quality ingredients and results, but also a compelling and credible brand story, elevated consumer experience, strong online and offline communities, and overall ‘why’ to buy.”

The players

5 mentionedHarry's

Momentous

Fine'ry

Deeper

DedCool