Mass Beauty Has Momentum. Can It Maintain It?

For mass-market brands and retailers, that durability presents a clear opening as consumers become more selective in how they spend. With mass beauty outgrowing prestige last year, increasing 5% in dollars compared to 4% for prestige, and accounting for 67% of the beauty market in the United States, according to market research firm Circana, retailers are capitalizing on the moment by investing in artificial intelligence, upgrading stores, premiumizing assortments and expanding K-Beauty and wellness offerings.

An extensive consumer base is a growth accelerant. Market research firm NielsenIQ estimates that 76% of U.S. beauty shoppers have purchased from Walmart, underscoring how mass retail transcends income brackets. American Enterprise Institute research cited by The Wall Street Journal shows 31% of Americans fall into the upper middle class, up from about 10% in 1979, yet many still feel financially stretched, reinforcing cautious, value-driven purchasing behavior.

Peri Edelstein, senior partner and managing director at Boston Consulting Group, says, “The mass channel has become more appealing for shoppers to get newness that wasn’t there in the past. We expect mass beauty to play a critical role in the category, especially as you see the lines blurring between traditional beauty and wellness. The mass channel is well set up to deliver against that and may even have an advantage.”

Few forces illustrate both that opportunity and the mounting pressure like Amazon’s rise in beauty. Fueled by the e-tailer, where price, convenience and replenishment are maximized, online now comprises more than half of beauty sales, intensifying competition for traditional mass retailers.

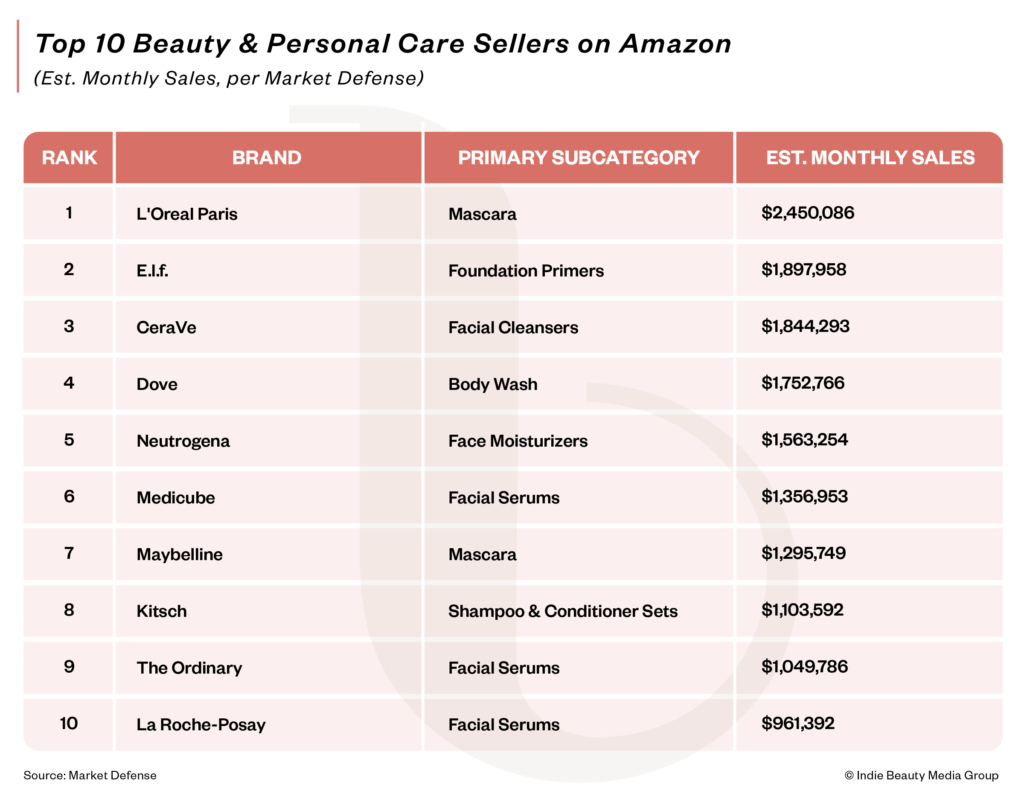

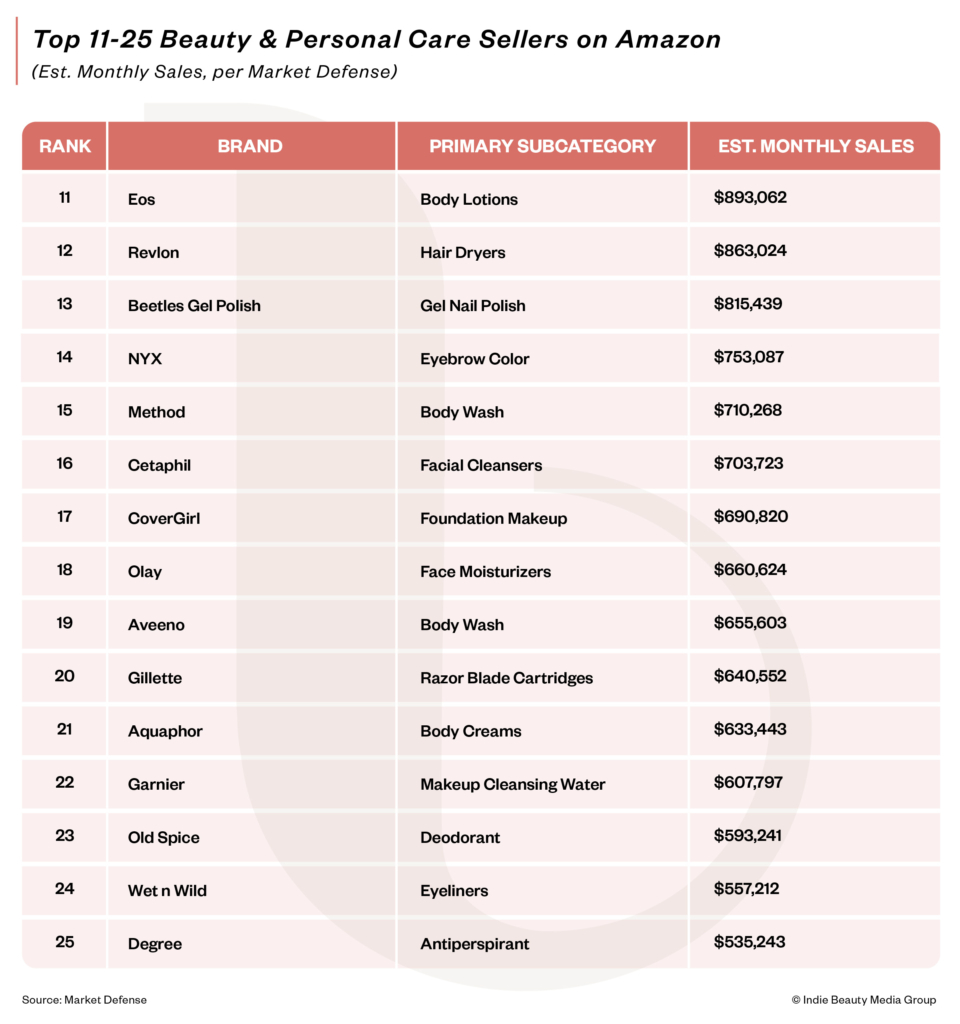

Looking at the top-selling beauty products on the platform, the dominance of everyday, replenishable items is apparent. Brands like L’Oréal Paris, E.l.f., CeraVe, Dove and Neutrogena rank among the top sellers by units, spanning products such as mascara, cleansers, body wash and moisturizers.

TD Cowen projects Amazon’s share of the U.S. beauty market will climb from 9% in 2023 to 15% by 2030, far outpacing gains from other players. The investment bank expects Walmart and Target to remain largely flat, while TikTok is forecast to reach 4% by 2030, up from 2% this year. NIQ estimates TikTok’s share as higher, at around 6%.

Raina Vaughan, VP of sales for retail sales management firm Team Direct Management, says, “Customers might discover something on TikTok, but they often want to buy it where they already shop and where it’s easy to replenish. TikTok Shop has added pressure for brands to move fast, but retailers are still looking at velocity, repeat and long-term performance.”

The competitive dynamics are shifting as price, the historic delineator between mass and prestige beauty, becomes less distinct, and masstige, the tier where the two intersect, commands a meaningful share, from 7% in fragrance to 16% in haircare, per Circana.

Larissa Jensen, SVP and global beauty advisor at Circana, identifies fragrance, facial skincare and personal care products such as body lotion, body wash and deodorant as propelling growth in mass retail, benefiting from consumers prioritizing self-care, elevated routines and wellness-oriented products. She says, “We expect these categories to stay strong in the coming year as shoppers continue looking for affordable products that feel good and work well.”

Across beauty retail, Jensen points out that online shopping and value-focused channels are gaining dollar share, while pure-play e-commerce, dollar stores, clubs and off-price are pulling share from other retail channels. She says, “Pure-play e-commerce is on track to maintain double-digit growth over the next year, and if trends hold, this channel could become the industry’s largest by 2027.”

Mass’s Makeup Problem

Mass beauty’s growth isn’t besting prestige beauty’s growth in every category. Prestige haircare and makeup grew 8% and 4% last year, double the pace of their mass counterparts. Should beauty enter a stronger makeup cycle, as many industry executives and analysts expect, the imbalance in makeup could be particularly problematic for mass.

Makeup tends to favor prestige, where brand cachet and innovation play an outsized role and the price gap with mass is relatively narrow. Mass accounts for roughly 45% of makeup sales, close to prestige’s 46%, but has struggled to capture momentum.

A key issue is innovation or lack thereof. Although mass makeup brands are pumping out new products (see Wet ‘n’ Wild and NYX’s Winnie the Pooh and Simpsons collaborations, respectively, and the latter’s The Face Unglue makeup remover balm and Maybelline’s Lifter Gel Oil-in-Gel Lip Gloss), fewer have broken through, and development cycles have lagged behind faster-moving indie and prestige players.

“Mass market is a bit of a mixed bag,” says Vaughan. “Innovation this past year has lagged behind prior years, with fewer big launches happening both within existing brands and across new brands. The segments seem to be a little stagnant.”

Legacy brands have weighed on mass makeup performance in some cases, notably Coty Inc.-owned CoverGirl. E.l.f. and Milani have been conspicuous exceptions, riding on rapid product development, strong value positioning and on-trend releases, though E.l.f.’s growth has begun to moderate from earlier highs.

Sydney Wagner, an equity analyst at investment bank Jefferies, says, “While E.l.f.’s innovation and nimble supply chain remain advantages, they can’t fully offset challenges in mass makeup channels. You’re not seeing the same pace of innovation from mass legacy brands across the category as you are from indie players, which tend to be more concentrated in prestige. That said, the potential expansion of K‑Beauty beyond skincare and into color cosmetics could provide a tailwind for mass.”

Coty has been looking to offload its flagging makeup assets, but in the meantime has been trying to address their issues, including with a stockkeeping unit rationalization plan to concentrate attention on hero items and innovation. However, Wagner explains, “Innovation has been cannibalizing rather than additive.”

Revlon is putting in effort under the direction of Michelle Peluso, the former CVS EVP and chief customer and experience officer, who understands mass-market retailing. Wagner says the brand has had “moments with nostalgia and lip trends,” but must shore up digital marketing and innovation to avoid losing mindshare in a competitive market. The lip category could be promising for Revlon, as it was one of the few strong makeup segments for mass retailers. Circana data for the 52 weeks ended Feb. 26, 2026, shows lip sales rose 6.7%, buoyed by a dramatic 36.2% increase in eyeliner sales.

Dupes have been strong as well. Influencers have normalized lower-priced alternatives to prestige products, and brands such as E.l.f., Milani and MCo Beauty have built businesses around offering similar aesthetics at accessible price points. Market research firm Future Market Insights estimates dupe sales reached $4.1 billion last year and could grow to $14.8 billion by 2036.

Jeremy Lowenstein, CMO of Milani, which has notched 17 consecutive quarters of growth, remarks that sustaining growth is becoming more challenging in the market overall. He says, “We are entering a more disciplined phase. Growth is still there, but consumers are shopping more intentionally, evaluating performance and brand trust more closely than ever.”

Mass Fragrance’s Dupe-Driven Revival

Dupes from brands like Dossier and Fine’ry have changed mass market’s fragrance game, proving that fragrance can sell in self-service big-box environments. For more than a decade, celebrity fragrances or designer scents nearing the end of their life cycle collected dust on discount and drugstore shelves and were often locked away.

Target posted fragrance sales gains for the 52-week period ended Feb. 22 of more than 45%, according to data obtained by Beauty Independent. CVS is coming on strong, too, with fragrance sales up more than 24%, and fragrance sales at Walmart are up double digits.

Vaughan notes that, along with fragrance dupe brands, Sol de Janeiro has spawned its own dupes from NatureWell and Holler and Glow that have been strong performers.

Coty introduced the Origen fragrance collection exclusively on Walmart’s website last year, and incubator Maesa, bolstered by the success with Mix:Bar, Being Frenshe and Fine’ry in mass doors, has unveiled Scents Unearth’d, a new fragrance line rooted in curiosity, discovery and authentic cultural storytelling that’s exclusive to Target. Revlon and Authentic Brands Group have inked a fragrance licensing deal for future fragrances in mass.

The challenge for mass-market players will be to anniversary the explosive growth of fragrance dupes and achieve sales momentum beyond dupes. Dupe brands such as Dossier are trying to carve out space for their own creations.

Mass’s Skincare Bright Spot

If there’s one category where the mass market glows, it’s skincare. Skincare delivered a 6% gain in mass last year in both dollars and units, versus 3% in prestige. Brands with clinical positioning and dermatological heritage have been winners.

CVS has long been a supporter of lines including Avène, CeraVe and La Roche-Posay, and the drugstore chain has tapped dermatologist Camille Howard as an advisor. Walmart is adding La Roche-Posay to about 1,500 doors.

The mass market’s ability to jump on K-Beauty is critical in skincare to lure shoppers who might otherwise flock to products and brands in the category at Sephora and Ulta Beauty, which have been K-Beauty collectors. According to NIQ, U.S. K-Beauty sales hit $2 billion in the 52 weeks ending Aug. 9, 2025, increasing 37.2% year over year from roughly $1.5 billion and far outpacing the broader beauty market’s single-digit growth.

Target has been aggressively growing its K-Beauty stable with brands like Round Lab, Cosrx, Skin1004, Haruharu Wonder and Numbuzin. CVS has stocked products from South Korea since the first K-Beauty wave. The chain’s current assortment includes House of Joseon, The Face Shop and Peach Slices.

Vaughan says, “Within skincare, acne and treatments continue to be drivers. The customer is continuing to discover classic favorites like Noxzema as well as K-Beauty favorites like Hanhoo and Peach Slices.”

Mass Retailers’ Beauty Offensive

Walmart, Target and CVS are working to elevate their beauty departments, ensuring assortments reflect key trends and making them easier to shop. Still, an industry expert notes that beauty doesn’t always command top priority at mass chains given it’s relatively slow-turning, space-intensive and typically accounts for less than 10% of total sales.

In a choppy economy, Vaughan says, “Retailers are being a lot more cautious right now. Instead of flooding the shelves with new brands, they’re really focused on productivity, what’s actually turning, what earns its space and what helps simplify the shop. There’s been a bigger push into adjacencies and clearer storytelling at shelf versus just adding more SKUs.”

Walmart is emphasizing a simpler shopping journey, artificial intelligence, clearer product benefits, sharper pricing, wellness-oriented merchandise and premium offerings. Over the past year, it has introduced more than 70 new beauty brands, including Dabble & Dollop, Liva, Nude by Nature, California Naturals, Pacifica, Gem, Bali Body, Blvd & Co and Odele. NielsenIQ reports that 76% of U.S. beauty shoppers purchase from Walmart, while TD Cowen estimates it holds roughly 20% of the domestic beauty market.

“The consumer right now is very value-focused and also much more informed,” says Vaughan. “Efficacy, trust and price are key in determining what they are buying. They want products that work. They don’t want to spend a ton of time figuring out what to buy or worse yet waste money on something that won’t satisfy their needs.”

She adds, “Walmart still has opportunity to grow with a more affluent consumer. While they have gained share within this consumer base over the last five years, they still have headroom to grow and will continue to focus on adding category-driving, premium brands to close that gap.”

The retailer is leaning into AI to support decision-making and free up teams to focus on the customer experience and loyalty. Roughly 1.6 million associates have access to AI tools, and its AI assistant Sparky is already shaping behavior, with users seeing basket sizes about 35% higher.

Walmart is encouraging brands to think beyond individual channels and instead plug into its integrated commerce ecosystem, where customers move fluidly between online and stores. Its online Marketplace functions as a lower-risk entry point for testing demand and expanding assortment.

Beauty Bars, in-store service stations offering hair, nail and makeup treatments, have expanded from a small pilot of 35 doors to plans for 450 nationwide. Sales in stores with the Beauty Bars have doubled in those doors, according to Vinima Shekhar, VP of beauty merchandising at Walmart, who spoke at a recent CEW event. The beauty department is being moved to the front of stores as new stores and remodels open.

CVS is moving skincare to the front of the store, streamlining shelves to ease shopping and amplifying service. Along with those efforts, it broadened Epic Beauty Sales, its limited-time promotional event, to more than 30 Navarro stores in Florida. The sale was promoted in Spanish and English across multiple marketing channels. A minis experience launched in 2,700 stores will expand this summer with new minis from Lume, Vacation, Batiste and others.

Target’s Life After Ulta Beauty

Target’s post-Ulta shop-in-shop approach is evidence of mass retailers’ premium beauty push in an increasingly competitive beauty landscape. The brand is rolling out Target Beauty Studio in stores with more than 60 high-end brands. Beauty advisors will assist in the shopping experience.

Target, which has onboarded over 60 beauty and wellness brands so far this year, including Hanhoo, Heyhae, Kundal, Elizavecca, Minimalist and Onside, is also opening Baby Boutiques to offer specialty-store shopping in 200 doors. Both the premium beauty and the baby boutiques will sell items in stores and online. Target is linking the upgraded assortments to its loyalty program, and beauty shoppers will receive targeted rewards through Target Circle.

Jeffrey Ten, longtime beauty industry executive and brand developer, says Target has “plans to add more niche brands to create a point of difference. Their new layouts suggest a shop-in-shop concept similar to Ulta, but all owned by Target. They have reached out to many people they have worked with in the past who are building startup brands and they are nurturing these small brands to be ready for distribution in Target.”

Founder-led brands will be a prominent part of the shop-in-shops. JR Little, VP of Crème Collective, a brand building company, says, “Many years ago, skincare brands were from big conglomerates but sometimes they didn’t have that tight social connection with their followers in the community. So, I really think it’s a big win for Target.”

Little concludes, “If they get the experience right, this could reshape how consumers think about buying beauty and provide prestige beauty brands with another major retail partner.”