Luxury Beauty's E-Commerce Conundrum

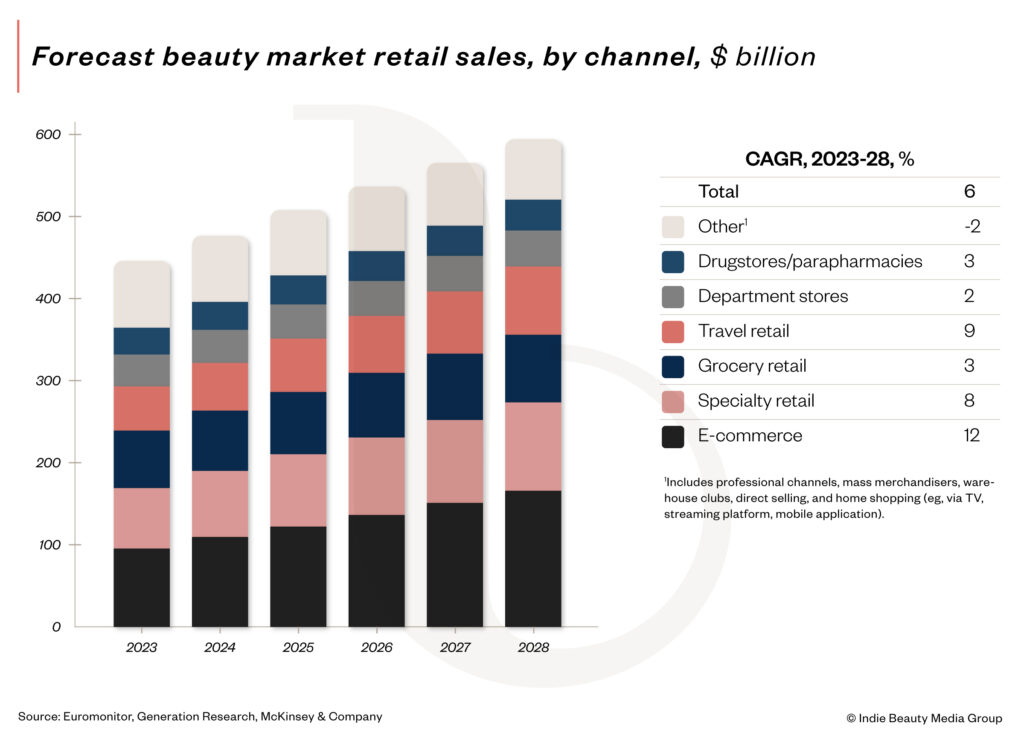

Scanning the e-commerce landscape, many beauty industry experts conclude there’s no pure-play online retailer with significant volume effectively selling luxury beauty. The e-tail beauty blunders have less to do with luxury beauty, which consultancy McKinsey & Co. projects will register the highest growth of any beauty subsegment through 2028, than the global conditions of luxury commerce and fashion. Beauty’s smallest subsegment, luxury beauty accounts for 4% of worldwide beauty sales.

Contraction of the personal luxury goods market—consulting firm Bain & Co. estimates it slid 1% to 3% in the first quarter 2024—financial mismanagement, competition from specialty retailers and Amazon, e-commerce’s post-pandemic reset and diminished attention to ancillary beauty assortments with lower ticket items than clothing and jewelry have doomed beauty’s presence in pure-play online luxury retail. McKinsey estimates online beauty purchases grew 8% versus specialty retailers’ 14% growth last year, but predicts e-commerce’s growth will outpace growth in all other sales channels through 2028.

Prior to Net-a-Porter’s decision to switch to an affiliate model, a move first reported by publication Women’s Wear Daily earlier this month, Farfetch shuttered its beauty operations last year. Farfetch owner Coupang sold luxury beauty e-tailer Violet Grey back to its founder Cassandra Grey and private equity investor Sherif Guirgis in the summer. Publication Puck News initially broke the news of Violet Grey’s sale. With a limited beauty selection, luxury e-commerce destination Ssense lumps beauty under its “everything else” merchandise tab. Moda Operandi entered beauty last year and remains in the category.

Contending with the distribution crunch, industry experts theorize luxury beauty brands will double down on standard channels, including direct-to-consumer websites, partnerships with brick-and-mortar retailers and standalone stores. They will also further extend abroad to markets like the Middle East with emerging luxury customer bases. However, the diminished strength of pure-play gatekeepers that can spark fascination in luxury beauty brands the way Violet Grey did with Augustinus Bader compounds the pressure on brands to erect their own distribution and marketing machines.

“It is just sad,” says Catherine Bossom, founder of beauty brand consultancy Yellow Flamingo. “There’s no Matches anymore either. I don’t think that anybody is necessarily going to pick up those brands because all of them are also retailed in places like Harrods, Selfridges and SpaceNK. I think the luxury element for those brands remains with those luxury retailers who have a store presence and then the brands being able to create that luxury environment within their own website. For brands, it was more about the positioning element of being on Net-a-Porter.”

Still, Aaron Chatterley, co-founder of teen skincare brand Indu and Feelunique, the British e-tailer that sold to Sephora in 2021, posits that Net-a-Porter’s retreat from beauty won’t have much effect on luxury brands’ sales in the long run and there are sufficient opportunities for luxury beauty brands. “If they’d had a meaningful share of the market, then it strikes me that they wouldn’t be retreating, they’d be expanding,” he says. “I think the international luxury beauty market is very well served by the current mix of physical and online players like Sephora, Douglas and their own direct-to-consumer channels.”

Net-a-Porter’s shedding of beauty wholesale comes after it narrowed its beauty selection amid profitability struggles. The e-tailer has registered consistent annual losses of more than 200 million euros or about $223 million a year, according to the publication Business of Fashion. Parent company Richemont, owner of Cartier and Van Cleef & Arpels, has been looking to offload it for the past few years.

First quarter sales at Yoox Net-a-Porter encompassing Net-a-Porter along with Mr. Porter, The Outnet and Yoox declined 15% at constant exchange rates. Sales dropped 11% in the previous quarter as the e-tailer battled a “challenging environment for pure play online distributors,” per Richemont.

Despite beauty’s e-commerce growth, Bossom argues luxury fashion retailers have never been able to grasp selling beauty online. “You have to over-invest. Beauty is more than just a purchase,” she says. “It’s about the experience you get. It’s about the content that comes with it. It’s about education. You could also argue that beauty online has become so commoditized that it just becomes about price. So, if I’m buying a product at one website, then I’m just going to buy it from somewhere else.”

Marc-Antoine Barrois, a luxury fragrance and scented candle maker with products in Bergdorf Goodman, Neiman Marcus and Harrods, points out that online luxury retailers are often hobbled by discounters. Beauty, especially, is affected by discounting.

“As soon as one player discounts a product, even by one cent, it appears among online search results,” he says. “So, as the number of players offering the same products increases, the acquisition cost of a client becomes more and more expensive. Unlike fashion where luxury retailers can offer exclusivity to their clients, within beauty they have to fight with the exact same offer as their competitors without really much service to offer.”

Elana Drell-Szyfer, CEO of premium skincare brand RéVive, highlights mounting competition as an important culprit in luxury e-tailers’ beauty stumbles. “There are more online options diverting from them like TikTok Shop and affiliate models, and the consolidation of bigger players who have stronger cash flow models to be able to sustain themselves,” she says. “You have the potential of Saks and Neimans and the question is, what does that mean for their online businesses? That’s a place where Saks has leaned in.”

In July, Saks Fifth Avenue parent company HBC acquired Neiman Marcus Group for $2.65 billion following years of attempted mergers between the two flagging department store companies. The acquisition created Saks Global, a retail group consisting of more than 150 Saks Fifth Avenue, Saks Off 5th, Neiman Marcus and Bergdorf Goodman stores in the United States. Amazon, a minority investor in the deal, will support the newly minted company’s technological and logistical capabilities.

The effect that Amazon will have on the combined company in the long run isn’t clear, but Saks Fifth Avenue’s e-commerce business Saks, which it spun off in 2021 in an attempt to achieve solvency, is currently in trouble. Saks has had liquidity problems, leaving scores of vendors in the lurch with unpaid bills.

Speaking of the the Saks Fifth Avenue and Neiman Marcus merger, Drell-Szyfer says, “Hopefully, they start to improve on the total omni-experience and create a brand differentiation between the two. We need them, and the customer is still spending money, so she needs a place to spend it.”

She adds, “You also have Amazon, too, but I don’t think that becomes a discovery destination for luxury beauty brands. I think it’s a replenishment destination, and I think the luxury of it is the convenience. You don’t go on it to launch a brand or build a brand. I think you do it to serve your customer.”

Amazon has made serious strides in boosting its premium beauty selection this year, onboarding Estée Lauder-owned prestige brands Clinique, Too Faced, Bumble and bumble and Smashbox as well as L’Oréal-owned Kiehl’s and emerging brand Evolvetogether. Separately, Amazon’s luxury offering across fashion, accessories, jewelry and beauty hasn’t been making serious strides. It features 26 brands—Dr. Barbara Sturm, Chanel, Edward Bess, Celine and Cle de Peau Beaute among them—while premium beauty features over 500.

Industry experts believe selling luxury beauty brands online isn’t simply about listing products. It’s dependent on creating an immersive, elevated experience for the customer. “The storytelling requires video, copy, narration, an authoritative voice as well as brand partner voices,” says Drell-Szyfer. “There is a lot of movement back in store by gen alpha, and a lot of demand for experiences in luxury like in travel and health and wellness. I don’t think luxury brands necessarily need a wholesale presence, but they do need some kind of introduction to the customer in an offline way.”

Barrois is emphatic that luxury beauty needs brick-and-mortar support to thrive. He says, “I personally never accepted pure online players if they were not the digital facet of a beautiful store.”

The players

5 mentionedClinique

RéVive

Smashbox

Kiehl's

Violet Grey