The Brutal Economics Of Beauty Specialty Retail

Brands are being forced to think carefully about the economics of wholesale distribution, from contribution margins and inventory turns to velocity, promotional spending and hero-product productivity, amid fierce competition for shelf space. Industry experts argue that founders often underestimate the millions of dollars needed to launch in specialty beauty retail within the first year.

Beauty retail consultant Lane Barrocas, who formerly held leadership roles at L’Oréal, LVMH Louis Vuitton Moët Hennessy and Coty, says specialty beauty retail is an expensive brand-building and customer acquisition channel that demands years of ongoing investment before financial returns trickle in. Breakeven commonly doesn’t occur until year three or four. Barrocas figures brands entering Sephora or Ulta should have $3 million to $5 million allocated for the first year alone to cover inventory, sampling, displays, shelf talkers, field staffing, marketing programs, promotions, loyalty participation and external brand marketing to support sell-through.

“I almost think of Sephora and Ulta as marketing spend and not a retailer,” he says. “You will not make money there if you’re doing it the right way. You have to have an investor behind you…willing to lose money for the first few years to be able to scale.”

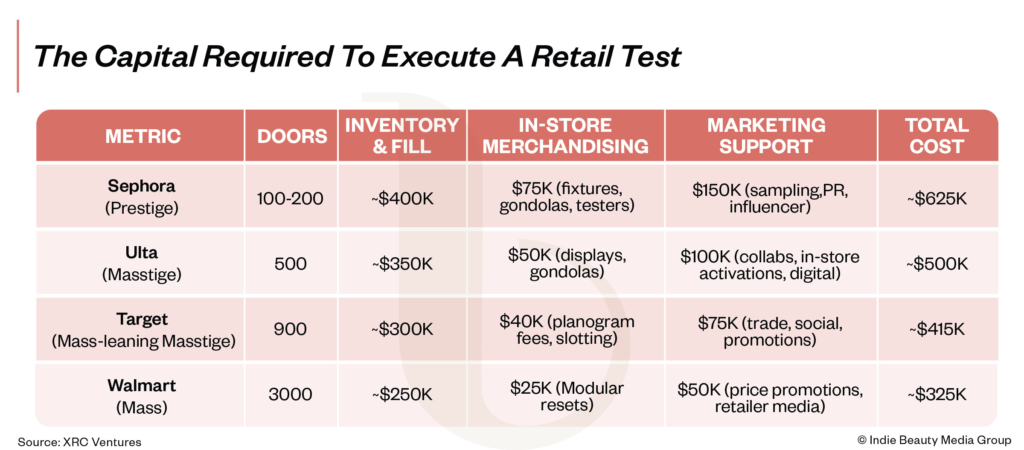

Brands participating in phased retail rollouts that encompass anywhere between 100 and 500 specialty doors tend to have lower upfront investments, roughly in the range of $500,000 to $700,000, estimates Kelly Chen, an investor at early stage venture capital fund XRC Ventures. She notes that investors generally expect emerging beauty brands under $5 million in sales to be unprofitable during the early stages of scaling. At Sephora, there are only a handful of brands that launch without outside investment or corporate ownership.

“By the time they get to that five to $10 million mark, then it’s like, all right, you should be hitting break-even to slight profitability around that mark, and then by the time you’re over $10 million, it’s like, yes, you should be profitable at that point,” says Chen. “You get to $20 million and almost every investor is expecting you to have double-digit EBITDA margins.”

XRC, backer of Billie, Naked Sundays and Solawave, evaluates brands by looking beyond basic product margins and assessing the profitability of each retail relationship after accounting for co-op marketing, chargebacks, tester costs, slotting fees, payment processing, returns and fulfillment expenses. Chen says many startups still focus almost entirely on top-line sales or gross margin percentages, but investors focus on contribution margin by channel and product. She stresses, “Gross margin is just the tip of the iceberg.”

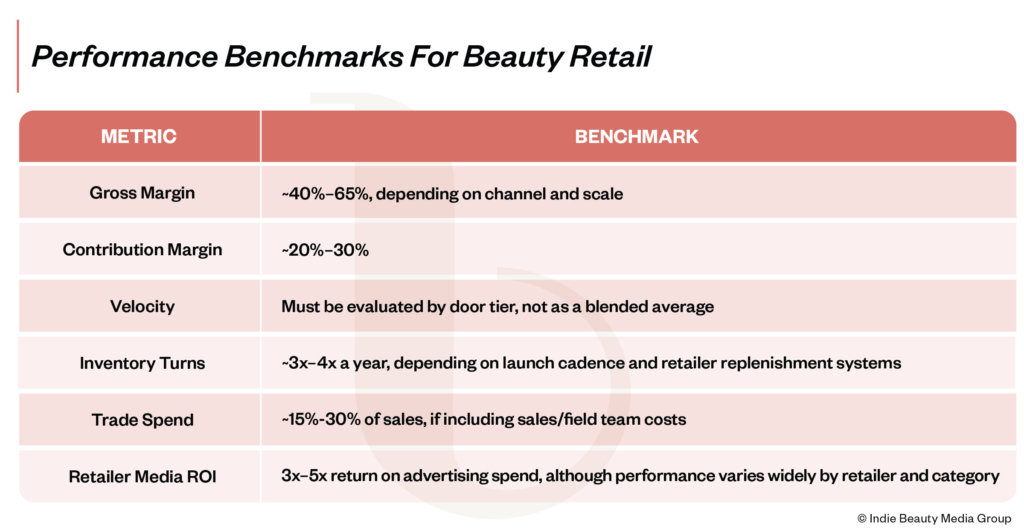

Depending on the channel, gross margins for beauty brands at retail can land anywhere from 40% to 65%, with specialty retailers typically demanding higher percentages. Contribution margins, or the amount of revenue left after factoring in all of the variable costs associated with selling a product or operating a channel, largely range from 20% to 30%. Barrocas says, “This is the real profitability signal in wholesale.”

Healthy inventory sell-through is usually three to four times a year for prestige brands, depending on launch cadence and retailers’ inventory systems, while trade spend typically is about 15% to 30% of sales, if brands deploy sizable field teams to service their specialty stores. Otherwise, the rate can be lower.

Velocity is another critical metric in beauty retail. Chen says investors increasingly assess brands based on relative category performance rather than total sales alone. For example, a sunscreen brand may have entirely different productivity expectations than a moisturizer or body care brand inside Sephora, making category-relative velocity one of the clearest indicators of a brand’s retail health. She also points out that higher-margin products aren’t always the most profitable if they move too slowly. A lower-margin product with significantly faster turns can propel greater contribution dollars for brands.

Chen says, “Your category will likely determine your turns, your velocities and what’s normal…which then determines how long your cash is going to be tied up as the inventory is just sitting on shelf.”

Velocity rates can differ greatly door to door and category to category, making it challenging to measure by a single industry average. “In prestige, it follows a power curve,” says Barrocas. “When I ran Lancôme at Macy’s, this was typical: the top five to 10 doors can do $3 million to $10 million annually. The top 50 doors often do about $1 million each. Bottom doors can be as low as $75,000 per year.”

As brands optimize for profitability, they should zero in on the productivity of their hero products. Barrocas argues that beauty retailers now want leaner assortments, more productivity and clearer merchandising stories centered on hero products capable of sustaining velocity. He identifies Rhode as an example of a brand successfully leveraging a tightly edited assortment and hero products to generate strong productivity at retail.

“The days of having 50 SKUs, 100 SKUs…those are done,” says Barrocas. “Narrow and deep is the way to go.”

Operational execution is ultimately one of the key determinants of retail profitability. Chen says many digitally native brands underestimate how dramatically retail changes the operational pressures placed on packaging, merchandising and logistics. Products designed for direct-to-consumer distribution may fail to maintain momentum in physical retail if they cannot display properly on shelf, communicate their value proposition quickly enough or receive sufficient in-store support. Scaling in too many doors too quickly is another common threat to profitability. Chen says, “That’s a big mistake that I see a lot of people do.”

Barrocas singles out Dillard’s as a profitability driver for beauty brands due to slower promotional cycles and its stable operating structure. He lists Bloomingdale’s, Nordstrom and QVC as similar. Chen underscores that successful beauty brands must diversify distribution risk and be omnichannel.

“Omnichannel is the best place to be longer term,” she says. “That’s where you could be the most profitable…if you’re in multiple channels and you’re using DTC and social media to drive awareness of the brand and then using some of these brick-and-mortar companies to scale.”