How Beauty Retail Assortments Are Being Recalibrated To Shore Up The Bottom Line

Faced with underperforming products and pressure to slash costs, several retailers, particularly in the prestige arena, have pumped the brakes on new brand launches this year and are depending on multimillion-dollar anchor brands like Augustinus Bader, Supergoop, Charlotte Tilbury, Westman Atelier and Dr. Barbara Sturm with proven track records of sales and strong followings to contribute to top-line and bottom-line growth.

Department store companies Neiman Marcus, Saks Fifth Avenue and Von Maur, clean beauty retailers Credo, The Detox Market and Clean(er) Beauty, and e-tailers Net-a-Porter and Shopbop have dialed back new brand introductions considerably. The beauty retail universe isn’t completely devoid of newness, however. Specialty and mass-market chains are injecting it carefully. Sephora has picked up Hello Sunday, Dieux Skin, Soft Services, Salt & Stone, Dr. Idriss Skincare, Iris & Romeo and Bread Beauty Supply, and Target has onboarded more than 10 brands.

Still, the deceleration of new brand additions serves as a wake-up call to any emerging brand thinking that omnichannel distribution encompassing a retail component is an easy ticket out of direct-to-consumer woes. And it should serve as a wake-up call to retailers, many of which are already not luring shoppers off the couch because they’re not viewed as exciting, differentiated destinations. The walk back from up-and-coming brands is causing their assortments to become a sea of sameness.

Sarah Broyd, partner at consulting firm Clarkston Consulting, points to economic uncertainty last year and elevated interest rates as reasons for retailers’ reluctance to tap smaller brands. While interest rates are slated to decline this year, consumers are expected to pull back on skincare and makeup purchases, although they’re still inclined to splurge on products they deem worthy of the investment.

“There’s some protectionism that’s happening when they look at brand allocations in stores right now,” says Broyd. “If there’s a huge boom in the economy again that’s when I think you’re going to see more experimentation. Retailers will be more willing to take a risk on a product because they’re doing well from a financial standpoint.”

In the current environment, Shelby Olsen, head of client and business development at Beauty Independent parent company Indie Beauty Media Group, explains retailers are banking on tried-and-true brands as a number of the hottest trends amid the pandemic’s e-commerce surge have calmed. “During COVID, there was an influx of incredible new and emerging beauty brands, and retailers were eager to change up their assortments and adjust to the times,” she says. “Consumers were shifting their focus back to natural, good-for-you brands and that often meant purchasing the smaller and more unknown products.”

In contrast to new brands, Olsen says an anchor brand is a “guaranteed ‘buy’ if they stock that brand online or in-store, not to mention future replenishment purchases. Every retailer wants these brands because they produce over and over again. Retailers are relying on these trophy brands to produce their top sales.”

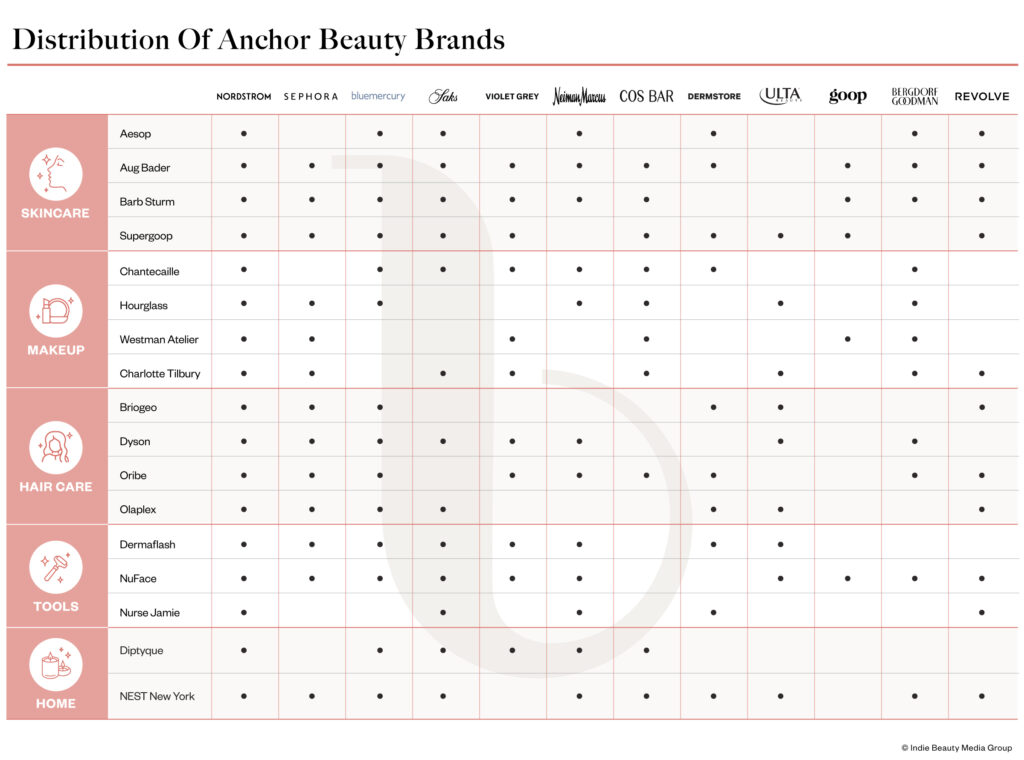

The impact of the reliance on proven players is evident in the overlapping brand rosters of big beauty retailers. Across 17 beauty brands prevalent at retail, including Augustinus Bader, Charlotte Tilbury, Westman Atelier and Olaplex, Nordstrom’s and Sephora’s beauty assortments overlap on over 75% of them. Sephora’s and Bluemercury’s beauty assortments overlap on nearly 65% of the brands, while Saks Fifth Avenue’s and Neiman Marcus’s beauty assortments overlap on approximately 52%.

Kelly St. John, founder and CEO of beauty brand consultancy KSJ Collective, figures that beauty retailers have been in what she refers to as an “edit-to-add” period for the past 18 months, meaning a new brand is only brought in if another brand is on the way out. So far, the approach has netted positive results for prestige beauty. According to market research Circana, prestige beauty sales climbed 14% last year to reach $31.7 billion.

“Productivity metrics have been established by [retail] leadership, and buyers are faced with the difficult task of exiting brands who are below the productivity line,” says St. John. “Since the pandemic years, most merchant teams have shrunk, so they have less resources and less attention to devote to emerging brands…Open-to-buy budgets, marketing dollars, space and location are being allocated to the brands who are hitting those productivity thresholds and who are demonstrating the ability to scale. The reality is that new brands are often not in the black with a retail partner until year three.”

Sephora stores in the United States have waved goodbye to JLo Beauty, and the retailer’s partnership with Clinique has waned. It’s removed the legacy brand from select stores and cut its shelf allocation in others. Target no longer carries brands such as LoveSeen and Reina Rebelde.

Olsen notes that the terms dictating the business relationship between retailers and emerging brands has been changing of late. Digital outfits like Flip and Thirteen Lune are operating with drop-ship and consignment models that place the burden of inventory costs on brands. When retailers place wholesale orders, they tend to range between three and 24 items per stockkeeping unit for brands rolling out online and at stores, per St. John. She says retailers have gotten more conservative with average opening orders for emerging brands in recent years and are slower to roll them out to stores.

Stephen Letourneau, chief brand officer at BFYW, a brand holding company with Mango Moi, Better Suds, The Ideation Lab and Stephen James Curated Coffee Collection in its portfolio, believes that retailers’ moves away from wholesale models are contributing to emerging brands’ retail struggles. “Instead of receiving payment for the complete order, retailers are paying for items sold weekly or monthly. Brands are shipping out 5,000 to 10,000 items and getting checks for $100 to $300 at a time,” he says. “You simply can’t reinvest at that level, so indie brands are getting pushed out of retailers. This leaves the conglomerates as the only ones who will be able to afford retail space.”

Karen Hayes, founder of brand consultancy Indie Global Strategies, forecasts that emerging beauty brands will confront a “shakeout” at retail this year as costs to compete mount. She says, “You never know when the algorithm is going to gift you with virality, but I think the feeling is that a lot of these brands are going to run out of money and are not going to be able to sustain a livelihood, let alone achieve profitability.”

The cost of launching at a big beauty retailer has increased precipitously over the last five years. In 2019, industry insiders pegged it around $250,000. Now, the cost can run up to $3 million depending on the brand, its launch strategy and the retailer’s footprint. Account setup at mass-market retailers alone can cost a brand as much as $50,000.

With once-buzzy retail concepts like Neighborhood Goods, Showfields, Standard Dose and Shen Beauty gone from the retail landscape, St. John highlights Bluemercury’s The Cache program as a vehicle for emerging brands looking to scale at a large beauty retailer. Launched in late 2022, The Cache features three to six new emerging brands every quarter. Brands selected for its assortment gain distribution online and in Bluemercury stores.

St. John says, “They have not only created a program that is focused on emerging brands, but that supports those curated handful of brands through dedicated merchandising, marketing support, priority education and mentorship.”

Letourneau identifies Pop Up Grocer as an innovative retail outlet that caters to rising brands. Begun as a traveling pop-up concept stocking products in the food, beverage, home, beauty, wellness and pet categories, Pop Up Grocer opened its first permanent location in New York City last year. It partnered with Nordstrom last summer on a pop-up fixture in eight of the department store company’s locations.

With traditional retail challenging to penetrate, brands are leaning into spas and boutiques to expand their distribution networks and erect reputations with beauty industry professionals to convince retailers to take a chance on them. “Indie brands will start building up their war chests in order to legitimately show large retail that they can bring new consumers into their spaces,” says Letourneau. “If the bulk of retail is offering the same 30 SKUs, consumers will quickly become bored and migrate to spas and boutiques for their next fix.”

Boutiques can be highly valuable to emerging beauty brands. During a panel discussion at Beauty Independent’s Uplink Live show in January, Sandra Velasquez, founder and CEO of Nopalera, remarked that a San Diego boutique that the bath and body care brand is stocked in outperforms its business at Nordstrom, where it’s sold online. Makeup brand Minori Beauty has assembled a network of over 100 boutiques, spas and hotels through the wholesale platform Faire, where it’s experienced explosive growth. Fast-growing facial bar and aesthetics treatment businesses are becoming hotspots for distribution, too.

As beauty retail assortments narrow, Hayes is hopeful that fresh distribution avenues will surface for emerging brands. “We’re in a time of disruption with social selling and AI. I don’t think any beauty entity is really thinking about or coming forward with something AI-led that truly affects retail and shopping. I think that’s probably going to happen, and we just can’t see that yet,” she says. “I don’t see any slowdown in the consumer drive for discovery or wanting newness, so I think that there will always be opportunities for new indie brands.”

This story was updated on Friday, March 15.

The players

5 mentionedAugustinus Bader

Bread Beauty Supply

Olaplex

Better Being

AS Beauty